")

UAMN has followed the progress of the eVTOL “AAM Reality Index” with a keen eye since its inception back in February. There are hundreds of companies jostling for position in this fast growing and nascent industry. Therefore, consulting firm SMG decided to create the “AAM Reality Index” to follow these world companies’ development and in so doing, form a “Top 20” of the best and most promising.

After UAMN published an article in April asking how the chart had faired during the previous two months, some weeks later, it seems, SMG decided to update the Index on a more regular and hoped for monthly basis, given the speed of the Industry’s progress.

Previous UAMN articles on “AAM Reality Index”:

https://www.urbanairmobilitynews.com/air-taxis/return-of-the-aam-reality-index-what-has-changed/

https://www.urbanairmobilitynews.com/research/read-report-review-index-rating-for-aam/

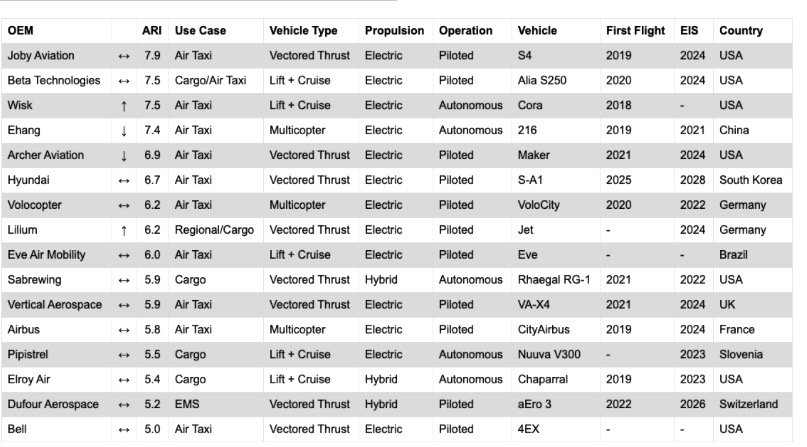

The most up-to-date chart for May shows a number of “movers and shakers” from February. These include:-

: EHang down 3 places.

: Joby moves up one to top spot.

: Wisk (up 1), Archer (down 1).

: Lilium is the biggest mover (+ 4), rising from 12th to 8th position.

The present May chart followed by the previous February positions

The person who decides is SMG’s, Sergio Cecutta, and below is a recent interview with him, published in newatlas.com. The journalist asking the questions is Loz Blain. The interview is very long as it looks at all aspects of the emerging eVTOL industry, so is published in two parts.

___________________________________________________________________________________

Blain: Let’s start with this: what is SMG and what are you guys trying to do here?

Sergio Cecutta: We are a consulting firm that basically works on aerospace, defence, and automotive – especially what’s called today, auto tech; that would be autonomy and electrification in cars. We work on the growth side of the house. Companies that want to launch new products, new markets, understand new geographies, pricing, supply chain, funding, M&A (mergers & acquisitions), that is what we do.

So, we are a group of experienced executives. All of us are engineers, as well as people that have run large businesses in corporate America. Since 2017, with the launch of the first Uber Elevate summit and the white paper,we started to get interested in this market. That interest turned into getting to know more and more about this market. We work with airlines, OEMs, suppliers, as well as aftermarket companies.

And one of the things that we started thinking to ourselves was, well, this is an interesting market, there are a lot of entrants, how do we make heads and tails of all these entrants? That’s the reason the Advanced Air Mobility Reality Index was created. So we created these tools for ourselves, and then we figured that, really, the industry was asking for these tools. This is the reason we publish and share them with the industry.

As a journalist, I get stacks of press releases from companies that are getting into this space. There are so many companies that want to be making eVTOLs, how do you evaluate these things when you first run across them?

We’ve decided to look at five different dimensions. One of our goals is to keep it simple and have something that is easy to compare. We wanted something that people can quickly understand, especially people from outside this space. It’s not like conventional aerospace where people are familiar with the brands. I mean, I don’t know anyone that doesn’t know a Boeing or an Airbus, they might not know which one they’re on, but they know that they’re out there. In the eVTOL space there is a lack of legacy players, but an abundance of start-ups. And so we looked at five dimensions.

Number one is funding. So, how much funding does the company have? Do they have enough to complete specific milestones in their development? Do they have enough to build a prototype? Do they have enough to certify? Do they have enough to enter service?

The second piece is their team. Not just the CEO, but is the leadership team an aerospace leadership team? Are they familiar with the industry? Do they know what it means to certify an aircraft? Have they already run programs of this size, this complexity?

The third piece is technology readiness. Now, we wanted to stay away from judging the design of an aircraft for two simple reasons: one, the aircraft are very different from each other, and two, really no one knows all the details, unless you’re inside the program. So we use what NASA uses – that is the technology readiness level (TRL) scale, it’s basically a scale from one to nine that looks at the maturity of the technology. Anything less than six is not ready for prime time. TRL 6 is the first time that a prototype has been flown in the relevant environment – a full-size aircraft that has covered the entire flight envelope. So, it has taken off vertically, it has transitioned, it has flown and it has landed. TRL 9 would be the final product.

The next piece that comes along is certification. Do they understand the certification requirements? How far along are they? Certification is very important, for the simple reason that the rules for certifying these vehicles are brand new, and no one has done it before.

Last but not least, we look at production, and the reason we look at production is because the manufacturers of these vehicles are talking about thousands of vehicles. In aerospace, we don’t make anything in the thousands. Take Airbus, they’re starting to think at a rate of about 60 A320-family aircraft a month. That’s what, about 700 aircraft a year, and that is a lot. But in the eVTOL market, people are talking about producing 900, 1,000, 1,500 a year. We’ve never heard of those kind of numbers. So, we wanted to see what’s their capability? Can they make one? Can they make ten? Can they make a hundred? Can they make thousands?

We’ve applied weights for each of these dimensions. And, while I’m not going into the secret sauce of the calculations, basically all of these elements combine to create a number.

Last but not least, the index does not try to say who’s going to be the winner. We don’t know. The index is a current snapshot of where we see the race being at right now. It’s a snapshot of how the different companies rank with respect to each other. Will it be different tomorrow? For sure. We published our latest update Monday, and I can tell you that I already have updates to that update! But again we’ll wait for a little more information to come along. It is a very dynamic space.

So, how often will you be updating this list?

The goal is to be monthly. We want to avoid having two to three month gaps, because there’s always enough information, but at the same time, we don’t want to bombard people with releases.

Certification, as you say, is a massive, massive challenge for any company that’s trying to get into this space. The numbers that I’ve heard off the record for what a certification run is going to cost – I’ve heard half a billion dollars, I’ve heard up to a billion dollars – just to get a single airframe certified, because it’s such a new space. The rules are not just new, as I understand they’re still being decided upon as this process proceeds. So, you’re looking for budgets around that level? What says to you that a company has enough money to do this?

Unfortunately, the devil is in the detail. The certification budget depends on two things: their supply chain strategy, and the type of vehicle they’re trying to certify. So, you have heard correctly, for some of the most complex configurations, they’re talking about a billion US dollars to get to certification. For some of the simpler ones, they’re talking about a quarter to half a billion.

Now, the truth is, we need to understand the complexity of the configuration. For example, multi-copters are less expensive to certify than more complex configurations like lift plus thrust, or vectored thrust configurations.

The other piece is the supply chain. So, if the company decides to go fully vertical, as in they will produce everything in-house, they need more money, because all the components need to conform and need to be certified, and all the burden will come back on that same company. If instead, they use a typical aerospace strategy for supply chain, as in to have risk-sharing partners, then each one of the partners will take a piece of the certification burden and the company will need less money.

So, unfortunately there is not one number that fits them all in. That is very important to understand.

Can you give me an example of a company that is sharing that risk in an appropriate way?

Well, for example, Honeywell is working as a risk-sharing partner with Vertical Aerospace,based in England. They’re making a vectored thrust aircraft, and Honeywell is providing the avionics and the flight controls for this specific vehicle. In this case, when it comes to risk-sharing, for the certification of the avionics and flight controls, that onus will fall on Honeywell, and not the manufacturer. Therefore, the amount of funding needed to arrive to certification in this case might be lower than if someone was making the flight controls in-house.

And it’s always good to have someone that can help. Any time you can retire risk, it’s a good thing. It makes it more likely that the program will follow the schedule that you have in mind.

So just to be clear, you guys have no business relationship with any of the companies on this list, you’re independent in that sense?

Correct.

OK, then let’s discuss some of the contenders!

When I first saw this list, eHang was on top of it. But in the latest version of the list they’ve moved down a couple of spaces. I was surprised to see them up on top given some of the news that came out lately. There was a short seller guy running around taking pictures of their facilities and chasing up contracted customers and basically trying to discredit the organisation. So, can you talk about what’s happening with eHang in the context of the index here?

When it comes to the short seller, without going into detail, claims like these need to be founded in proof. And usually what we see is that if there is an involvement from the SEC, that is the Securities and Exchange Commission in the US, then we worry about claims, but usually if the SEC doesn’t get involved, it means that they do not consider the claims to be something that they have to worry about. You’ve seen the SEC step in, for example, with Nikola. We’ve seen it with other companies.

When it comes to eHang, they have a specific market in China. And right now if you look at these companies, there is really no alternative. Yes, Volocopter has announced that they will be working with Geely, one of the largest car manufacturers in the world and one of their investors, but at the same time, having a position in China is very important. And it’s also a market that could be closed to outsiders. eHang does have a vehicle, and now they’re actually expanding their portfolio to include other vehicles, and if you look at all of the dimensions and you calculate according to the numbers, you will see that they do come up in the top 10.

Do you guys see an easier path, perhaps, to certification in China?

Well, I don’t know if it’s easier, but it’s going to be a specific path. Until now. China has always used or adopted regulations from either EASA or FAA, and in this type of vehicle, it could be that China will be more of a pioneer when it comes to certification. So, it could be a different set of rules. Speculating is pointless, because there are so many variables. But again, what matters is that the CAAC is creating its own rules, they’re not waiting for FAA or EASA to finish with theirs.

So, top of your current list, and separated from the others by a bit of a margin there, is Joby Aviation. These guys were one of the first to get into this scene. What do you guys see when you look at that company?

Joby, they’ve been around since 2009, if I’m not mistaken, and they have developed multiple manned and unmanned aircraft. They have flown the entire envelope, and if you watch the video where they announced their SPAC, they have demonstrated that the vehicle is quiet demonstrated that the vehicle is quiet. And that is one of the critical aspects for these vehicles; they need to be significantly quieter than the vehicles that operate today.

The other piece that’s important is that they’ve defined a certification basis with the FAA. That basically means they have defined the list of requirements that they will have to meet for certification. Last but not least, they’ve obtained what’s called MFR: military flight release. Basically it’s a military airworthiness for their machine, and they share that only with one other company, Beta Aviation. In the industry, they’re seen as the leading companies when it comes to these kind of vehicles.

And Beta Technologies with the Alia, that’s second on your list there. They’ve just done a deal with UPS?

They’ve done a deal with UPS. They’ve done a deal with Blade. And as of yesterday they announced the reception of military airworthiness. There is a slight difference, because the military worthiness received by Joby was for the full envelope, but unmanned.

Instead, Beta has received military airworthiness only for its airplane mode, not the vertical mode. But at the same time it is the first manned airworthiness in this sector. That means that the Air Force is confident enough to put one of their pilots in the seat, and start to understand what it will mean to have electric aviation be part of the future of their portfolio.

In third place you’ve got Wisk Aero, obviously an offshoot of Kitty Hawk, and they’re operating primarily in New Zealand at the moment. What do you guys see when you look at Wisk?

So, Wisk has also been around for a long, long time, starting out with Kitty Hawk. Now they have a very strong partner on board in Boeing. It seems Boeing has chosen Wisk as their road to market. Right now they’re flying the fifth generation of their vehicle, and they are getting ready, by the end of the year, to come up with the sixth generation, which is going to be basically the production-representative aircraft that they will go ahead and certify.

Lately, they have opened certification both in New Zealand, and in the US with the FAA. And last but not least, you’ve seen yesterday an order from Blade for 30 of their vehicles. Now, Wisk is going fully autonomous, and that could mean a longer certification time, as opposed to manned aircraft, but as of this time we really don’t know what that means.

I guess it’s hard to talk about Wisk without bringing up Archer as well, which comes two spots further down on your listing in fifth place. Archer’s come in fairly late in the game with a lot of energy, a lot of money and perhaps from the sounds of things a bit of legal trouble in he form of that fight they’re having with Wisk.

Yeah. I mean, as far as the legal fight, that’s something for the legal system. But Archer does have an extremely talented group of individuals. They have put together the cream of the crop of the industry, and they are proceeding at a very good pace to bring these airplanes to market.

Now, one of the things that we don’t do with the index is to consider any of the SPACs. Those have been announced, but the deals have not been closed. They haven’t gone through the full scrutiny of the authorities, so when the deal will close you will see these companies trading publicly on a specific exchange. And that time has not arrived yet. For the three companies on our list that have announced SPACs, they all have spoken about the end of Q2, so probably it’s going to be around the June time period where we’ll see these deals close, and the cash will actually move into their coffers.

END (OF PART 1)

(Read Part 2 of this interview on UAMN located at the home page)